AI is reshaping markets and Fidelity’s Alex Wright thinks value investors stand to benefit most.

AI-driven sell-offs are creating valuation dislocations that reward contrarian stock pickers, according to Fidelity International’s Alex Wright, who has been adding to staffing companies and wealth managers he believes markets have indiscriminately punished.

Wright, manager of the Fidelity Special Situations fund and the Fidelity Special Values trust, said that sharp market dislocations caused by the rise of artificial intelligence (AI) are creating one of the most compelling backdrops for value investors in recent years.

Software has been at centre of these dislocations as investors fear rapidly evolving AI could destroy conventional subscription and enterprise software models. For example, IBM had its worst single-day decline since October 2000 on 22 February after Anthropic announced its Claude Code tool could modernise COBOL, the programming language underpinning IBM’s mainframe business.

Insurance and financial advisory businesses face similar pressure. The S&P 500 insurance index recorded its largest single-day decline since October after an AI-powered comparison tool launched on ChatGPT. Wealth management and data analytics firms came under pressure shortly afterwards when a rival launched AI-driven tax planning tools.

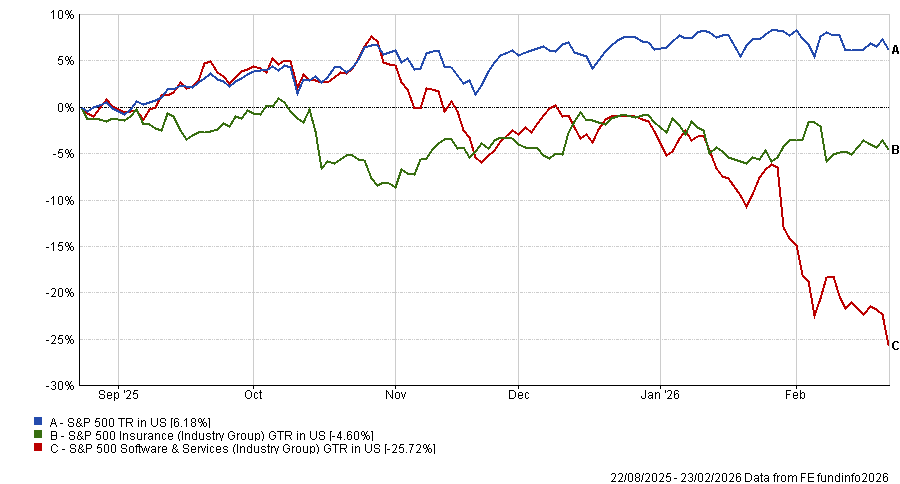

Performance of US sectors over 6 months

Source: FE Analytics. Total return in US dollars between 23 Aug 2025 and 23 Feb 2026.

Wright drew a direct parallel with the pandemic-era dislocation that preceded a strong recovery in unloved stocks.

“AI-driven volatility is reshaping markets. The last time it felt this opportunistic was during the Covid-19 pandemic, when many high-quality companies traded at deeply depressed valuations even as fundamentals began to stabilise,” he said.

“Similarly, the market environment today is presenting a wave of dislocation as AI developments ripple through industries and throw up pockets of investment opportunities. We also believe this uncertain backdrop increasingly tilts in favour of value investors going forward.”

For Wright, the main uncertainty created by AI disruption is valuation. Generative AI has made the 10-year outlook for many industries genuinely difficult to predict and that uncertainty falls hardest on companies priced for certainty.

“Companies trading on rich multiples leave little margin for error,” he said. “When investors assume a company’s monopoly advantage will endure, even a modest shift in competitive dynamics, including the risk of AI-driven disruption, can justify a meaningful de-rating.”

He has seen this dynamic play out in information services and software, where he said valuations had “rightly fallen from very high levels” but in most cases “still remain expensive”.

His response is to avoid businesses where stretched multiples are reliant on long-run certainty and to focus instead on companies with strong balance sheets where markets have overreacted to perceived AI risk.

Over the past six months, Wright increased his exposure to staffing companies, with Page Group, Robert Hays and SThree together accounting for 2.1% of Fidelity Special Situations’ portfolio. The investment case runs directly against market sentiment.

“Investors have viewed staffers as vulnerable to disintermediation long before the emergence of AI,” he said. “More recently, concerns about automation and job displacement have intensified those fears. However, we have yet to see clear evidence that AI has structurally impaired these businesses.”

Wright attributed the sector’s weakness primarily to cyclical factors: corporate caution and low candidate churn following the pandemic. Valuations have fallen below trough levels as a result.

However, he pointed to the US as an early indicator.

“In the US, where AI adoption is most advanced, we are already seeing signs of improvement in staffing activity,” he said. “The risk reward profile is very attractive over a three-to-five-year view as valuations reflect significant disruption, while offering substantial upside should a recovery in hiring activity materialise.”

Wright noted that wealth managers are the latest sector to be drawn into what he described as increasingly irrational market reactions to AI disruption. His holding in St James’s Place – which was caught up in the recent sell-off – illustrates the dynamic.

The sector has faced disintermediation fears before, from robo-advice and lower-cost alternatives, without suffering meaningful structural damage. Wright’s view is that the current AI-driven sell-off follows the same pattern: disproportionate punishment relative to actual structural risk.

Alongside businesses he believes have been unfairly sold off, Wright is also identifying companies with genuine AI-related tailwinds that remain underappreciated.

Outsourcing company Mitie, which supports the design and delivery of data centres, and integrated utility SSE, which benefits from greater demand for electric grids and renewable energy, both represent this category in his portfolio.

Neither is obviously an AI play, which the Fidelity manager suggested is precisely why the market has not fully priced in their exposure.

As a contrarian investor, Wright said he would normally grow more cautious when markets reach record levels but the current environment is different.

He argued there are early signs of an economic inflexion, particularly in industrial and consumer-facing sectors that have endured a prolonged period of weakness. However, he noted that, despite stabilising or improving fundamentals, many of these companies continue to trade at depressed valuations.

“At the same time, companies perceived to be sensitive to AI disruption have sold off sharply. Markets have indiscriminately punished anything with even indirect AI exposure, often without clear evidence of structural impairment,” he finished.

“Despite headline markets hitting all-time highs, it’s an attractive hunting ground for contrarian investment opportunities.”